Get Easy access to DBWC Latest news,

activities and events.

Download your app

Get easy access to DBWC latest news, activities and events.

Download our App Here.

When it comes to microfinance, the name of Nobel Prize-winner, Muhammed Yunus, always comes to mind. As the Founder of microfinance, he is the catalyst of economic change by accessing and unlocking the entrepreneurial spirit of unemployed and low-income populations. To his credit, the Grameen Bank in Bangladesh implemented microcredit as an innovative approach to traditional banking, which is essentially providing smaller loans to transform the unemployed into potential entrepreneurs. Ultimately, this became an innovative economic pillar for job creation. This is what defines microfinance today.

When it comes to microfinance, the name of Nobel Prize-winner, Muhammed Yunus, always comes to mind. As the Founder of microfinance, he is the catalyst of economic change by accessing and unlocking the entrepreneurial spirit of unemployed and low-income populations. To his credit, the Grameen Bank in Bangladesh implemented microcredit as an innovative approach to traditional banking, which is essentially providing smaller loans to transform the unemployed into potential entrepreneurs. Ultimately, this became an innovative economic pillar for job creation. This is what defines microfinance today.

In this article, we focus on the main basics of microfinance in term of: 1) Objectives, 2) Benefits, and 3) Challenges. Our purpose is to also show how Pi Slice overcomes the challenges of microfinance by engaging the private sector.

1. Main Microfinance Objectives:

Job Creation: Unemployed and low-income populations have potential small business ideas or vocational skills but lack access to funding. Microfinance provides these talented and skilled people enough funding and the opportunity to develop their idea or skill into a sustainable and profitable business.

Economic Stability: Microfinance provides unemployed populations with the opportunity to become micro-entrepreneurs, and therefore have a better income to be financially stable. As a result, those micro-entrepreneurs contribute to the growth of the private sector and stability of local economies.

Social Stability: Microfinance empowers the excluded segments of society, such as women and racial minorities, by enabling them to readily participate in the economic activity. In turn, these excluded segments become more confident and empowered, thereby promoting gender equality and decline of violence as well as vandalism.

2. Main Benefits of Microfinance:

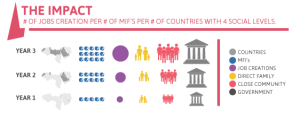

Social Impact: By financially supporting excluded beneficiaries such as women, farmers, handymen, etc, job creation for micro-entrepreneurs, has a direct impact on social stability at three levels:

Economic Development: By increasing the number of stable job creation and outreach, productivity, income, purchasing power, efficiency, financial management, profitability, empowered communities and gender equality, microfinance will ultimately result in advancing a thriving and sustainable private sector, and therefore the economy at large.

Innovation: By providing small loans to unemployed, low-income and excluded segments of society, microfinance nourishes the resourcefulness, creativity, determination and problem-solving skills of these populations to create innovative ideas that turn into profitable businesses.

3. Main Challenges of Microfinance:

Access to capital: How to channel alternative low cost funding to microfinance institutions in order to support them in expanding their services and micro-entrepreneurs portfolio?

Visibility: How to raise awareness to the public about microfinance in general as well as the work and impact of Microfinance Institutions (MFIs) in particular?

Transparency: How to inspire more transparency into the lending performance, accountability and operational processes of MFIs?

Overcoming Challenges: The Microfinance & Private Sector Bond

With the above in mind, we ask one important and timely question: Why is the relationship between microfinance and the private sector relevant to the MENA region? It is relevant because, historically speaking, there is a huge funding gap for MENA’s low income and unemployed populations that have the potential to become micro-entrepreneurs and contribute to the creation of approximately 3 million jobs. In fact, it is estimated that approximately 6 million households are eligible for microfinance loans, yet only 3 million have access to funding, which leaves approximately 3 million potential microfinance customers in need of funding for a total of nearly $3.5 billion in growth loan portfolio. The private sector has enough financial resources and channels that could contribute to reducing this gap. This is why Pi Slice’s mission is to engage and connect the private sector.

Pi Slice: Making a Difference

Pi Slice’s business model specifically targets the above gap by reaching out to the private sector as online corporate and individual lenders to support the ecosystem of micro-entrepreneurship. In other words, we serve the role of an online matchmaker between microfinance and the private sector by increasing the opportunities for micro-entrepreneurs to access capital.

In summary, Pi Slice offers an innovative online solution that engages the private sector in microfinance activities in order to effectively and sustainably achieve the objectives of microfinance and to deliver on its benefits through a lasting and sustainable impact on local and regional economies.

You too can make a difference now. Why not get involved and make life count with us at pi-slice.com?

Pi Slice Infograhic: http://visual.ly/pi-slice-infographic-2013

Get Easy access to DBWC Latest news,

activities and events.

Download your app